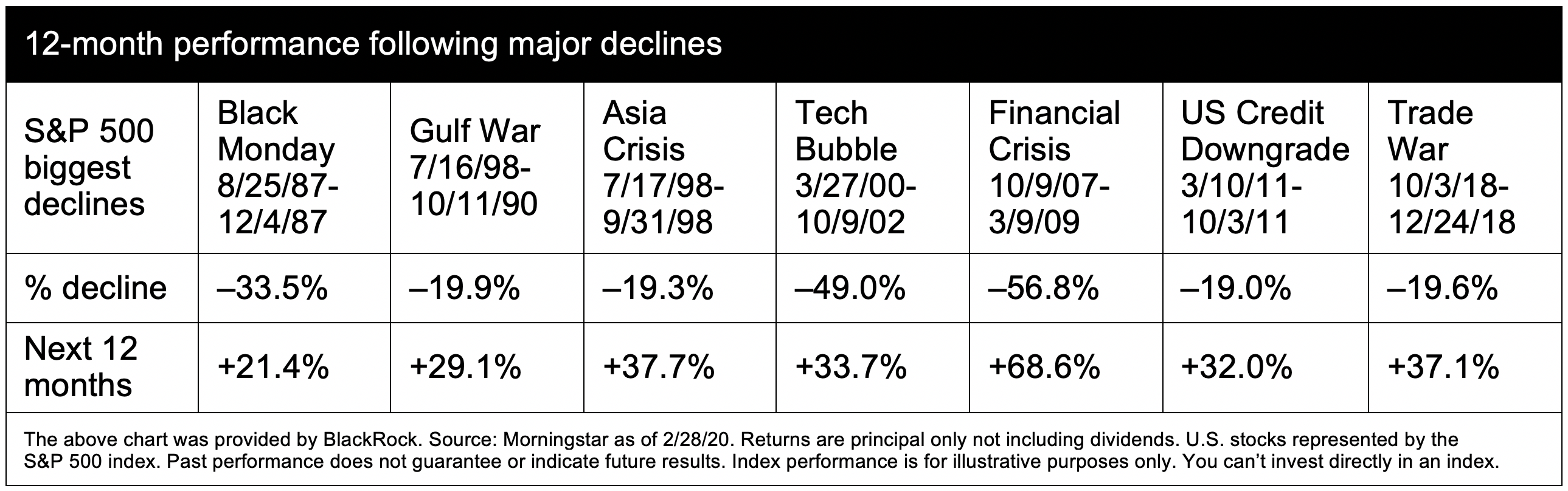

The continuing spread of COVID-19 and the uncertainty around the global economic impact, as well as the recent plunge in oil prices, has led to unprecedent market volatility and a sharp decline in the stock market.

Unprecedented action

The Fed has taken unprecedented action by reducing short term rates to near 0% as well as announcing a $700 billion asset purchase program concentrated on treasury and mortgage backed securities. Despite this action the S&P 500 is down 22% for 2020 and investors have fled to the safe haven of treasury securities, causing the 10-year treasury yield to decline 90bps to 1.02% and the 30 year treasury yield to decline 80bps to 1.63%. There has been evidence of mass liquidations and margin calls, reflected in unusual moves in U.S. Treasuries and credit markets. The fall in interest rates will negatively affect the discount rates used to value pension liabilities. Increasing credit spreads, an indicator of investor confidence in corporate credit, have softened the decline of discount rates.

As of March 13, discount rates for the Buck Yield Curve have decreased 24 bps. The fall in discount rates could negatively impact pension plans’ funding percentage. The exact impact depends on the plan’s asset allocation and the degree to which they have hedged the interest rate risk of their liabilities. Plans with low levels of hedging and a high allocation to high growth assets may find themselves in an even more challenging situation. It is our view interest rates will remain low for an extended period of time and it is likely that The Federal Reserve will engage in even more large-scale asset purchases.

Liquidity

First and foremost, plan sponsors need to ensure they have enough liquidity to meet benefits payments for the foreseeable future. History tells us investors have been rewarded that have the ability to stay invested throughout market regimes.

If assets need to be sold to generate cash, plan sponsors should make sure that the asset allocation remains in line with the investment policy statement. In addition, any portfolio rebalancing must account for the increased transaction cost, especially in the less liquid markets. Investors should be tactical with respect to raising cash accessing the markets when the tape is green.

If assets need to be sold to generate cash, plan sponsors should make sure that the asset allocation remains in line with the investment policy statement. In addition, any portfolio rebalancing must account for the increased transaction cost, especially in the less liquid markets. Investors should be tactical with respect to raising cash accessing the markets when the tape is green.

Understanding what and how much risk plan sponsors are taking in the portfolio relative to the liabilities is essential. Before a plan sponsor can take advantage of any market disruptions, they need to understand what “bets” they have on versus the liabilities. In order to quantify that risk Buck recommends performing an asset liability study.

Strategies

Plan Sponsors should closely monitor their plans funded percentage and quantify the potential size of required contributions if discount rates stay low and assets levels stay depressed. Plan sponsors need to also manage their cashflow and balance sheets and prepare for a multi-quarter recession.

Plan sponsors who are in an LDI strategy:

- Should make sure the interest rate hedge ratio does not need to be rebalanced as Convexity may cause liabilities to further outpace assets. As interest rates decline, durations – interest rate sensitivities – of assets and liabilities increase due to convexity;

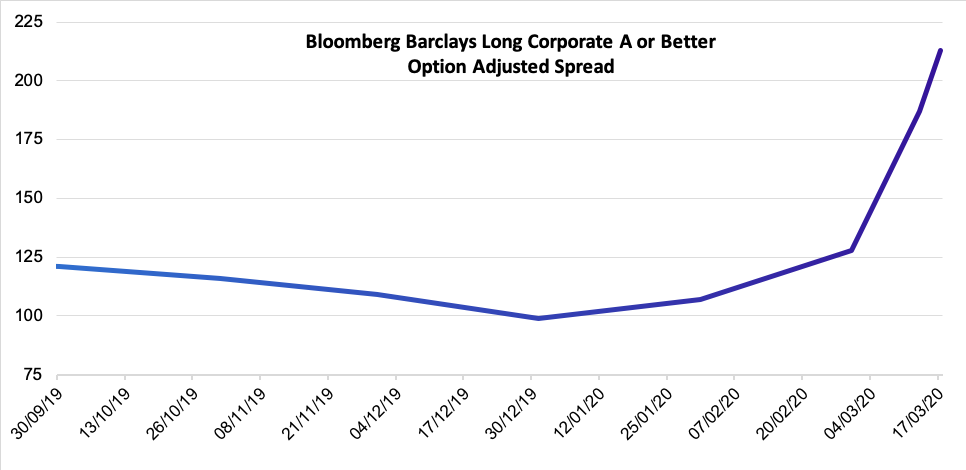

- May want to consider starting to hedge a greater per centage of their credit risk relative to the liabilities as credit spreads have widened and it is likely there will be a strong fiscal response;

Source: Bloomberg Barclays

- In times of credit stress Buck recommends employing an active management approach to credit/LDI investment management, as well having a strategic partner to help with the due diligence and selecting the appropriate asset manager to help the plan sponsor achieve their objectives.

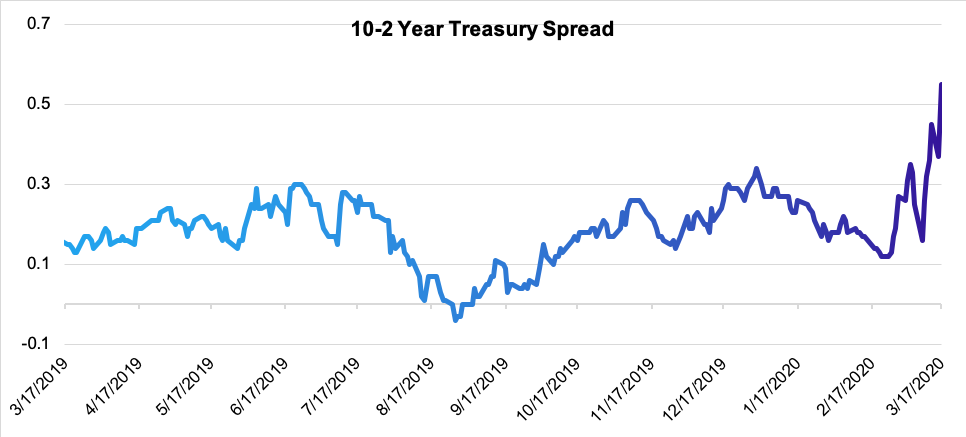

Plan sponsors with low levels of interest rate hedge should consider using synthetic strategies (treasury futures) to better hedge their liabilities as it will allow them to remain allocated to their Growth Assets. While the overall level of rates has decreased the yield curve has steepened further compensating investors to extend duration.

Source: U.S. Department of the Treasury

Plan sponsors should also closely monitor their investment managers performance and actions to ensure that their investment thesis is still valid.

For more information

For additional perspective on the market and the impact of COVID-19, register for our March 25 webinar on managing risk in an era of uncertainty. PIMCO market strategist Tony Crescenzi will join Buck’s investment team for a discussion on current market trends and the implications for plan sponsors and the capital markets.

This was written as of March 18, 2020. The investment products and strategies in this proposal are for presentation purposes only. This proposal does not consider your or your plans’ specific investment needs. This proposal is not a solicitation to buy or sell any investment, nor to participate in any type of trading or investment strategy. The purpose of this presentation is to illustrate hypothetical scenarios with respect to the funding and managing pension plans and other guaranteed benefits. Before making any investment decision, you should seek the guidance of a qualified financial or investment advisor such as Buck.