Let me tell you how it will be

There’s one for you nineteen for me

Cause I’m the taxman, yeah, I’m the taxman.

- George Harrison

Recently released federal and provincial budgets have once again shifted overall tax regimes, with much-touted relief to the middle class ostensibly funded by high-income earners who are now to shoulder a relatively larger share than they did before. Let’s set aside the political motivations of these changes for a minute and look at how they could influence compensation practices.

« RCA’s…clearly become far more attractive when tax brackets exceed that magical 50% mark. » Marc-Andre Vinson, Canadian IPP / Ottawa Market Leader

Suppose your company pays its top executives salaries and bonuses that put them well into that top marginal tax bracket (federally, that’s anything above $200,000, and it’s similar for most provinces, though for some it can be as much as $300,000). In several provinces – most notably in Ontario, Quebec, Nova Scotia and New Brunswick, that top rate is well above 50% and reaches at high as 58.75%. This probably doesn’t sit well with your executives. It also might lead you to consider alternative ways of compensating them that are more tax-effective.

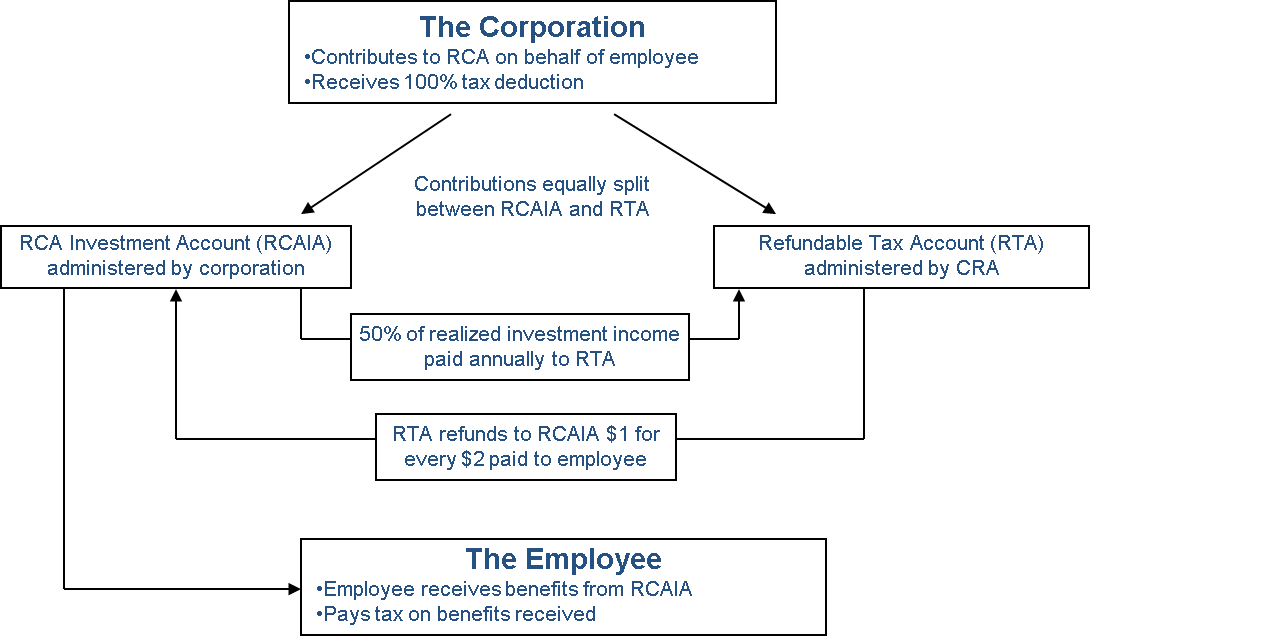

Retirement Compensation Arrangements could be the answer

Though it was originally designed to be tax-neutral, a Retirement Compensation Arrangement (RCA) could be one answer to today’s higher income tax rates. Contributions made by a company to an RCA are forcibly split, with half sent to an investment account, and the other half held by the Canada Revenue Agency in a Refundable Tax Account (RTA) that earns zero interest. However, once the executive retires and starts receiving benefits from the RCA, the RTA refunds half of all benefit payments and the money flows back into the investment account.

Not such a bad deal

With top marginal tax rates now exceeding 50% in several provinces, parking half of the retirement savings that compose an RCA isn’t such a bad deal, compared with the alternative of giving more than half to the Tax Man right away. The comparison only improves if your executive is expected to drop to a lower income tax bracket at retirement, which is not unusual since retirement income is often far lower than during active employment, especially for high-income earners.

As with any financial product, care should be taken up front to ensure that an RCA meets with the objectives of the individuals and the companies involved, and that everyone understands their rights and obligations.

RCA’s aren’t the only way to reduce the overall tax burden on executives, but they clearly become far more attractive when tax brackets exceed that magical 50% mark..