Volume 40 | Issue 03

Download this For Your Information as a printable PDF

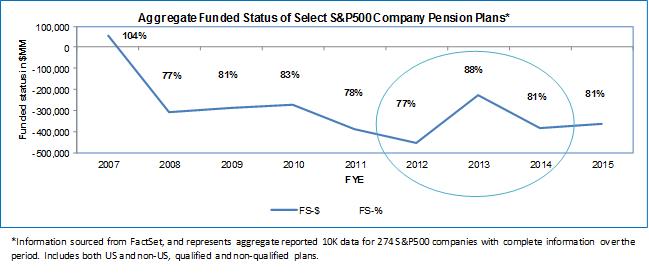

Events leading up to and in the aftermath of President-elect Trump’s victory have created tailwinds for pension plans: increased yields on both Treasury and corporate debt and rising prices across global equity markets. Additionally, as expected, the Federal Open Market Committee voted at its December 14, 2016 meeting to increase the key federal funds rate by one-quarter percent – and they signaled that further increases should be expected. These events generally have served to reduce pension plan liabilities and improve funded status. Sponsors should assess the impact of these events on their plans, and consider whether pension funding, investment strategies and risk management should be re-evaluated.

Background

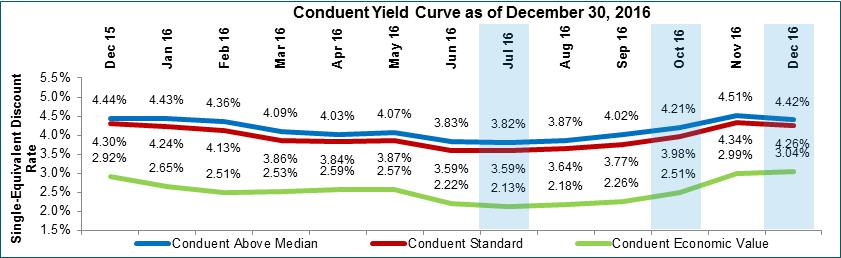

Immediately after the Brexit vote in late June, interest rates (as measured by bond yields) in the US reached historic lows while equity markets were underperforming year-to-date. As a result, many pension and postretirement benefit plan funded ratios declined sharply relative to reported measures at the beginning of the year, as we reported in our June 28, 2016 For Your Information. Shortly after the end of June, however, US bond yields began to rise as unemployment levels continued to decline and GDP growth levels continued to increase. The accompanying chart shows that, based on an average of 10 sample pension plan cash flows, the average discount rate in July 2016 was at 3.59%. In the months leading up to the US election, this average discount rate rose to 3.98%, while growth assets grew substantially.

Recent Developments – 2016 US Presidential Election and FOMC Vote

November 8, 2016 – Election Day – appears, at least in the short term, to mark a watershed moment for the US economy and interest rates in the US. Democratic nominee Hillary Clinton was widely expected to win the presidential election, and her expected policies were reflected in pricing of capital markets leading up to Election Day. As we now know, Donald Trump instead won the election, and we have since seen a rise in equity markets and bond yields, which continued through mid-December.

In addition, the Federal Open Market Committee (FOMC) voted on December 14 to raise the key federal funds rate by one-quarter point, to 0.50%-0.75%. This decision was expected, and the markets had priced a virtual 100% likelihood into Treasury futures prior to the FOMC meeting. However, in the accompanying statement and in remarks by Federal Reserve Board (Fed) Chairwoman Janet Yellen, the Fed forecast that the federal funds rate would be increasing three times in 2017, one more time than indicated by prior guidance.

Increasing the federal funds rate is a key lever used by the Fed to keep inflation in check. Signaling that they expected to increase the rate three times in 2017 indicates that the Fed believes the economy will grow at a faster rate than previously expected. In addition, the spread between conventional and TIPS bonds – an indicator of market expectations of inflation – dropped in the day after the Fed announcement, as the markets reacted to the Fed’s apparent intention to keep inflation under control and near the long-term target of 2%.

The one-quarter percent increase in the federal funds rate was already reflected in the short end of the Treasury Yield Curve in the days leading up to the Fed announcement. However, 10-year Treasury yields continue to rise. These increases were reflected in part in corporate bond yields – welcome news to corporate pension plan sponsors that are measuring liabilities as of December 31.

Good News for Defined Benefit Pension Plans?

It’s now eight weeks past Election Day. Between Election Day and the end of 2016, equity markets (as measured by the S&P 500 Index) increased approximately 5%. Thirty-year Treasuries have yields to maturity that increased 43 basis points; 10-year Treasury yields rose 57 basis points over the same period. Corporate bond yields are up a bit less than that – AA spreads are down about 25 points since Election Day – but this important curve for determining pension accounting liabilities is significantly higher than before the election. As of December 30, the single equivalent discount rates computed using ten sample plan cash flows stands at 4.26%, an increase of 28 basis points since October 31 and 67 basis points since July 31. Thus, although the value of bonds held in pension plans has decreased, pension liabilities have come down significantly and growth assets are exceeding expectations. By any measure, and notwithstanding the decreases in interest rates in the second half of December 2016, this has been good news for the typical under-hedged, underfunded pension plan. The specific impact of these post-election conditions on pension plans will vary based on each plan’s individual circumstances: asset allocation, funded ratio and liability duration.

What Plan Sponsors Should Consider

Plan sponsors now find themselves in a better position than they likely had expected, which may allow them to achieve their funding goals, or reduce risk, sooner than anticipated. They should consider some of the following strategies that might “lock in” these gains to potentially avoid a repeat of the roller-coaster ride taken as recently as 2013/2014:

Dynamic De-Risking

Dynamic de-risking is a technique that falls under the umbrella of liability-driven investing (LDI). Using this approach, a plan sponsor will build into its investment policy statement a series of asset allocations that gradually moves the level of risk lower as funded status improves. De-risking is programmed to occur when a particular funded ratio is attained. There are also variants where de-risking is set to occur when interest rates rise to a certain level, or based on a calendar approach, or sometimes a combination of these criteria.

Under a dynamic de-risking strategy, a plan sponsor takes more risks (including equity risks) when the plan is less well funded and there are economic benefits to taking those risks. When the plan becomes better funded to the extent that there is less economic benefit to incurring risk, the risk exposure is dialed back and prior gains are locked in.

Some plan sponsors have been reluctant to engage in risk reduction strategies such as dynamic de-risking for their pension plans, believing that interest rates would eventually rise and lift their plans out of deficit. Other sponsors have been interested in dynamic de-risking, but felt it was not the time to implement a de-risking glide path while interest rates were low and their funded ratios were so poor. And others have implemented dynamic de-risking, but their funded ratios have been so poor that they have not taken a step down their de-risking glide path yet.

With the recent rises in interest rates and solid equity returns, plan sponsors may find they are approaching a de-risking target milepost. Frequent (preferably daily) attention should be paid to funded ratios so as not to miss an opportunity to move down the glide path. Sponsors who may have considered and rejected a glide path in the past may wish to re-evaluate their decision in light of the current environment.

Annuity Purchase

One way to eliminate certain pension risks is to purchase annuities on behalf of all or a subgroup of participants. Often a plan sponsor will contract with an insurer to transfer the obligation to make future pension payments, in exchange for a single, up-front premium payment. Such a transaction transfers interest rate, investment and longevity risks for those participants to the insurer, while eliminating the associated plan administration costs, including PBGC premiums, which are scheduled to increase significantly over the next several years. Note that the decision to purchase annuities is a settlor function, but the selection of the annuity provider is a fiduciary decision.

Currently, a popular risk transfer strategy involves purchasing annuities for a subset of participants in payment status who have small monthly benefits (e.g., less than $300 per month), since these participants have disproportionately large fixed administrative costs, including PBGC flat-rate premiums (currently $69 per participant in 2017, and slated to increase to $80 in 2020 with indexing further upward from there). When the recognized balance sheet liability plus the present value of these fixed costs exceeds the group annuity premium, many plan sponsors conclude that it makes economic sense to proceed with the transaction.

By most indicators, annuity purchase rates have increased by about 50 basis points since November 8 and, at the same time, are at higher levels than for most of 2016. As such, group annuity purchases may be more feasible today for many sponsors, and transactions involving retirees with small benefit payments will likely continue to increase in popularity. It is important, nevertheless, to remember that annuity rates, and therefore annuity premiums, change daily and depend on a whole host of factors outside of a plan sponsor’s control, including market interest rates, insurers’ availability of capital and capacity, competition, and so forth. Therefore, plan sponsors who are contemplating a group annuity purchase should pay close attention to developments in this market.

Accelerated Funding

There are many positive benefits, both in terms of benefit security and absolute economics, to making voluntary contributions above those required by law. These benefits include tax-free accumulation of investment earnings within the plan, reduction or elimination of PBGC variable rate premiums, and the opportunity to take less risk. It is often the case that such a strategy has a demonstrably positive effect on earnings per share.

Non-Cash Contributions

An increasingly popular technique for funding acceleration is to borrow money (for example by tapping an existing line of credit, taking a bank loan, or issuing bonds) and using the proceeds to fund the pension plan. This is arguably a strategy that leaves the balance sheet unchanged – merely a “debt-for-debt” swap. In many circumstances, the borrowing cost for debt may be more than offset by the PBGC premium savings, even without the benefit of a deduction.

Note that because the increase in the federal funds rate is likely to lead to increases in borrowing costs, plan sponsors that intend to borrow money at a fixed rate (for example by issuing a bond with a fixed coupon) may wish to conduct these transactions as soon as possible, in case borrowing costs rise faster than the PBGC variable premium rate.

Alternatively, several sponsors have taken a more creative approach, by contributing company securities or non‑cash assets such as unencumbered real estate holdings. Such tactics may require independent appraisals, legal and fiduciary assistance (and prohibited transaction exemptions), but can also be extremely beneficial in the right circumstances. As always, the advice of counsel is highly recommended when entering into such complex transactions.

Offering a Lump Sum Window to Terminated Vested Participants

In recent years, a popular risk management strategy has been to offer lump sums to former employees. In doing so, a plan relieves itself of the per-head PBGC premiums associated with participants who elect the lump sums. In addition, because of the typical spread between GAAP discount rates and IRS prescribed interest rates under Internal Revenue Code Section 417(e), a plan can pay less to participants than the accounting liability on the books for those participants.

For plans with a lump sum rate under Section 417(e) that changes once a year, sponsors will find as accounting interest rates rise, the spread between accounting liabilities and statutory lump sums is shrinking – and the advantage of offering a lump sum window is diminishing. Plan sponsors that remain interested in considering a lump sum window to some participants, but have not communicated that decision to them, may wish to re-evaluate the decision to offer the window – and its timing – in light of the changes in economic circumstances.

Other Considerations

Regardless of whether any strategies are taken or revised in reaction to the change in markets, plan sponsors that have prepared forecasts (e.g., for budget estimates) before November may consider revising those estimates to incorporate the current interest rate environment and equity appreciation. In doing so, sponsors may wish to reflect the new mortality improvement scales that have been published by the Society of Actuaries (or variants that have been approved for use). The updated improvement scales generally forecast that longevity will improve over time, but not as fast as forecast using the prior scales. This will generally lower projected plan liabilities

In Closing

The recent gains in the stock markets and increases in interest rates are poised to give a boost to corporate balance sheets. But, as history has proven, nothing is certain, and what goes up often does come down. In fact, the drops in interest rates and the modest losses in the equity markets in the second half of December 2016 illustrate the importance of seizing opportunities to de-risk when they present themselves. Plan sponsors will want to continue to monitor developments carefully in the political and finance arenas during the presidential transition and beyond, and will want to consider taking steps to reduce costs and financial risk, now that the price of following these strategies has come down.