For Professional Clients Only

This article was written on 8 February 2024. It is a financial promotion and was approved by Buck Consultants (Administration & Investment) Limited, 9 February 2024.

Why new problems require different solutions

The 2023 Purple Book, published by the Pension Protection Fund (“PPF”) in December 2023, evidenced an enormous shift in defined benefit scheme funding. In March 2022, the projected shortfall measured against the cost of “buy-out”1, was over £440bn. By 31 March 2023 this had become a net surplus of nearly £150bn.

What caused this seismic c.£590bn improvement and what does this mean for trustees?

Cause

The Purple Book provides an annual update on the state of the DB pensions universe. Over recent years the data painted a gradually evolving, and from a funding perspective, improving picture.

The first Purple Book, published in 2006 before the Global Financial Crisis (“GFC”), showed that 88% of schemes were accruing new liabilities and investment strategies were largely focussed on growth. The GFC brought a new economic cycle of lows. Low interest rates to combat low growth and low inflation. The low yield environment drove large DB deficits and permanent changes to corporate DB pension provision.

While some industry commentators have characterised the 2023 Purple Book data as the end of DB, (I’ll leave for another day whether or not this is premature), today’s circumstances really began with the GFC. Many corporates elected to close DB schemes to new members, followed by future accrual.

Since the mid-2010s, trustees and sponsors have gradually been chipping away at shortfalls through significant deficit reduction contributions and strong growth asset returns. With fewer new liabilities being created funding steadily improved and the liability profile of schemes matured, with rapid increases in net cash outflows. Accordingly, asset allocation shifted from growth to protection strategies, for example with a major shift from equities to bonds.

In 2016 the Purple Book’s estimated shortfall relative to buyout was almost £1tn. By 2022, this had more than halved to around £440bn – still around 20% of FTSE All-Share total equity market capitalisation.

As Ernest Hemingway highlighted in his novel, The Sun Also Rises, bankruptcy happens in “Two ways. Gradually, then suddenly”. For the curious world of DB pensions, it would appear solvency follows Hemmingway’s adage. The decade up to the middle of 2022 saw only gradual progress, but since then we have witnessed a huge leap forward.

A new economic environment

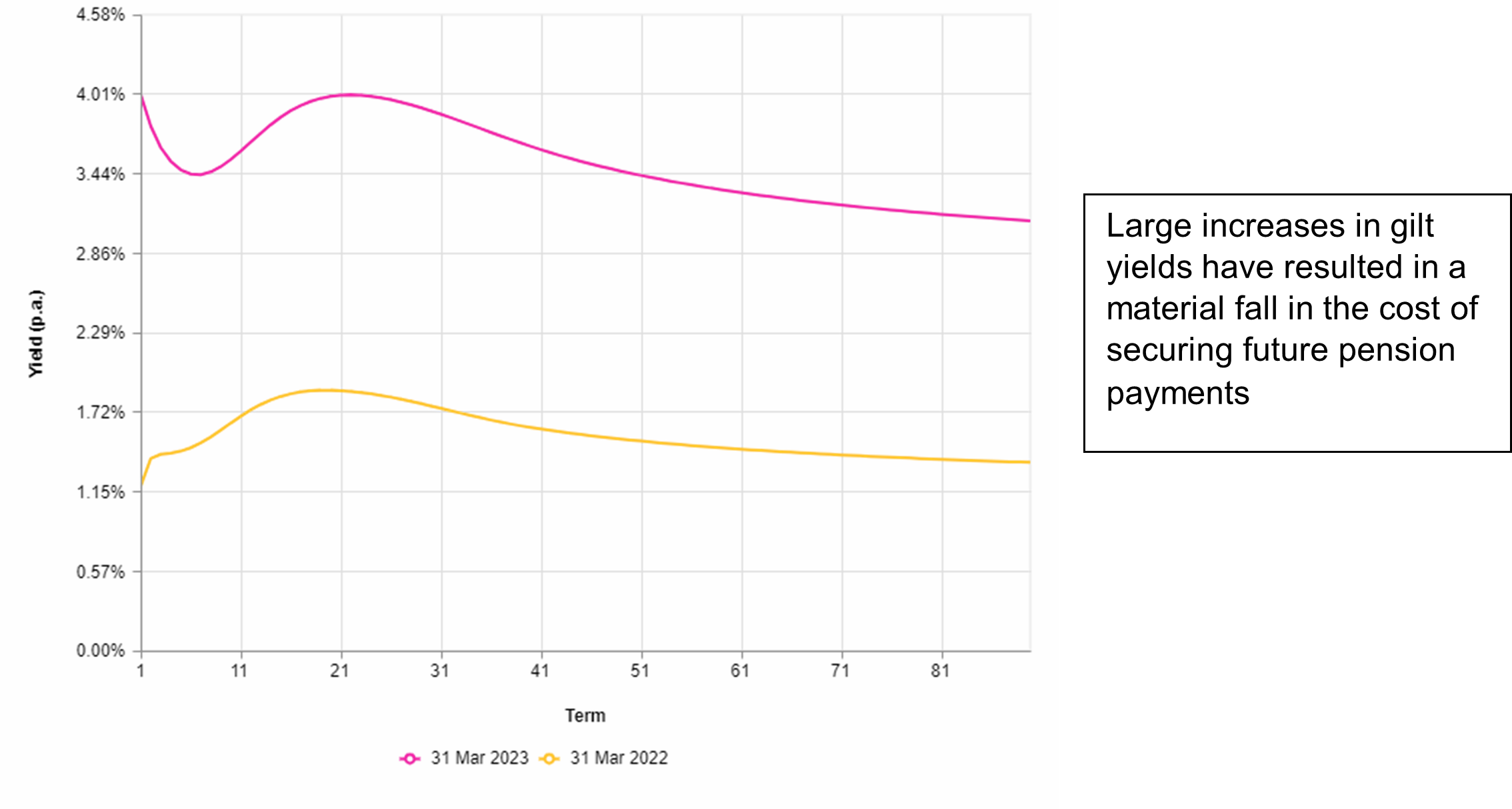

The leap forward is attributable to the marked change to the economic landscape since March 2022. The period captured a spike in inflation, driven by latent supply side disruption effects from COVID-19 and then war in Ukraine, all exacerbated by excess pent-up demand. This was followed by the autumn 2022 UK gilt crisis, ignited by Kwasi Kwarteng’s infamous mini-budget. These factors contributed to a significant rise in UK gilt yields, a key component of insurer annuity pricing.

Bank of England fixed interest gilt yield spot curve

Source: Bank of England, Buck

Source: Bank of England, Buck

And effect

As a result of rising gilt yields, the value placed on buyout liabilities fell by c.40% over the year to March 2023 (from c.£2.1tn to c.£1.3tn).

Asset values, in comparison, were estimated to have fallen by much less (c.16%), reflecting either outperformance within bond portfolios relative to liabilities, or non-bond assets outperforming bond assets (or a combination of both).

Cautious conclusions

It is worth noting that the Purple Book data, while measured at 31 March each year, uses asset and liability data gathered from various points over the preceding three years and projects forward asset and liability positions to the measurement date.

Given the scale of the upward movement in gilt yields, prevalence of leveraged LDI across asset portfolios and possible de-risking over the period (which may have seen the PPF underestimate an increase to interest rate sensitivity of asset portfolios), a significant health warning should be placed on overly precise conclusions.

Implications

However, while it’s reasonable to be cautious about the absolute level of aggregate surplus given underlying data limitations, the coal-face experience is that trustees and sponsors have indeed seen a substantial funding improvement for their schemes, with many planning and completing buy-in/buyout transactions.

Funding improvements on buyout measures have been driven by schemes in aggregate being “underhedged” relative to their respective buyout liability interest rate sensitivity. Hedging strategies commonly focus on Technical Provisions (“TPs”) measures, given these determine sponsor contributions. While schemes have been in significant buyout deficits (typical pre-autumn 2022) it was, in our experience, historically unusual to hedge materially beyond the asset base given this would introduce more volatility on TPs bases.

While Buyout funding levels leapt forward in the year to 31 March 2023, TPs funding levels may have seen less of an improvement, given relatively higher levels of interest rate hedging employed.

Where TPs deficits existed pre-LDI crisis it is likely these deficits are now much smaller (for similar reasons). For schemes with upcoming triennial valuations, there may be scope to adopt a more prudent funding approach (e.g., to align with a new Long-Term Objective) or reduce contributions if TPs are already in the Regulator’s Low Dependency range.

What to do

1. Trustees should ensure their investment strategy reflects new objectives and investment horizons.

At Buck, our cashflow centred investment philosophy encourages our clients to invest according to their investment time horizon. With buyout suddenly rushing into view, time horizons have materially shortened in many cases, prompting de-risking activities.

Plenty of activity took place through late 2022 and 2023 to lock-in funding gains. However, writing on 8 February 2024 it is clear opportunities remain.

As inflation has softened, but nominal yields remain persistent (albeit volatile), real yields sit 80-90 bps higher across the curve than as at 31 March 2023, meaning there may be further scope to reduce risk.

Bank of England 15-year gilt real yield

Source: Bank of England, Buck

Source: Bank of England, Buck

2. Maintaining resilience. Where strategic objectives now focus on managing a strong funding position with a low-risk asset portfolio, investment servicing should reflect this.

For schemes with minimal growth holdings, monitoring activities should be predominantly focussed on funding and cashflow risks.

For low-risk strategies, a “leaky” interest rate or inflation hedge is now typically a much larger proportion of total funding risk. Trustees should ensure that their hedging levels are not only aligned with their objectives both in terms of hedge ratio and term structure, but also the instruments used to construct the hedge.

Trustees should consider whether their use of credit, gilts, swaps and repos in their hedging arrangements is consistent with any short-term objectives for insurer transactions. Indeed, depending on the choice of insurer, the liability measurement yardstick in the run-up to a buy-in transaction may change. With gilt and swap spreads trading at high levels compared to recent history, there is material scope for a seemingly 100% hedged strategy to underperform the liability measure, revealing an unexpected deficit at an inopportune moment.

Monitoring credit portfolios should also focus on the key strategic functions. For example, where buy and maintain credit is held to match cashflows, it is important to monitor the evolving likelihood that the portfolio delivers the required capital to meet pension benefit payments, rather than, say, quarterly absolute performance. Monitoring credit fundamentals, issuance and evolution of credit spreads can help identify risks and opportunities where tracking performance against a stated benchmark may not.

Lower risk portfolios bring expectations of lower margins for error. Trustees should demand tools appropriate for this new challenge.

Important Notice: The article is generic in nature and should not be regarded as providing specific advice or a recommendation of suitability. No action should be taken without seeking appropriate advice, taking account of how the market environment has changed since the date of this article. There can be no guarantee that any opinions expressed herein will prove correct.

[1] The exercise to transfer all financial obligations of a pension scheme to an insurer. The cost of buyout is the premium payable to the insurer.