At the end of 2013, I was helping advise a trustee board, on which the company representative felt so strongly that interest rates were going to rise, that he wanted to sell the remaining hedging. His proposal was to move the whole index-linked gilts portfolio into property – commercial property, he reasoned, was only going to rise. In fairness, in absolute terms, property has done very well over the past couple of years so one can sympathise with the decision to invest.

However, this ignores the huge problem that was really causing the company a headache – the impact of interest rates’ movements on liabilities. Continually falling rates have resulted in widening deficits and painful conversations about contributions come Actuarial Valuation time.

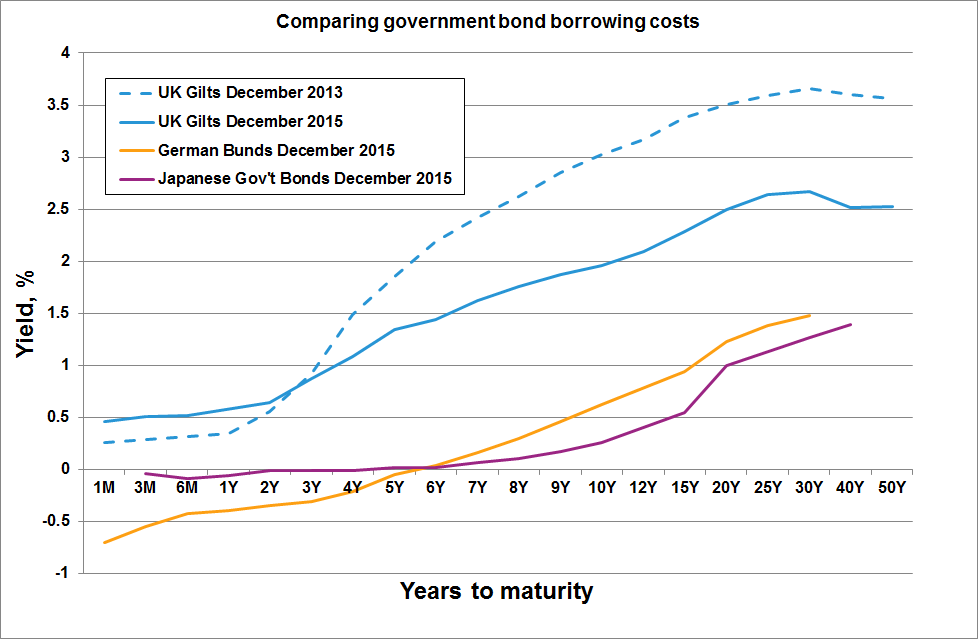

[ctt title=»As yields have continued to fall over recent years, a shift can be seen in market-wide interest rate predictions.» tweet=»Investment consultant @williamrwparry discusses market-wide interest rates in his latest blog post http://ctt.ec/rfKB4+» coverup=»rfKB4″] When speaking to clients about increasing hedging, including company representatives, I now see much lower resistance to the idea. This seems counter-intuitive. In 2013, when rates were far higher, many people were saying that yields couldn’t rise quickly enough. Now that they’re lower, more people want to lock in to these levels.

In order to try and explain this, it helps to look at the borrowing costs of other governments, such as Germany and Japan.

In the chart, you can visualise the tumbling effect as yields move from end 2013 levels, to where we are today, to where a low-growth, low inflation economy might take us. What has changed in the intervening period has been the seeping realisation of the implications of prolonged debt deflation and a 30-year adjustment to permanently lower inflation.

This message seems to be filtering through to pension schemes and companies – although the pain of rates falling has been considerable, the idea that rates can go even lower is more painful and no longer mere speculative forecasting.

I’m sure the trustees I mentioned earlier are now happy that the big property punt was over-ruled. It’s a brave trustee that looks at this chart and wants to unwind its hedging.

William Parry is an investment consultant in our London office. You can reach him by email or Twitter.