Volume 2017 | Issue 73

Download this FYI as a printable PDF

As part of the drive to improve pension scheme transparency, the Financial Conduct Authority (FCA) has published a policy statement providing rules and guidance to improve the disclosure of transaction costs in workplace pensions.

The FCA sets out requirements, for companies managing money on behalf of workplace pension schemes providing money purchase benefits, to disclose administration charges and transaction costs to the trustees and Independent Governance Committees (IGCs) of those schemes, using a standard approach. The rules come into force on 3 January 2018, as they relate to group personal pensions and other contract-based pension schemes.

Background

The FCA published a consultation in October 2016 on transaction cost disclosure in workplace pensions, which set out the series of measures that the government and the FCA have put in place to require greater transparency of costs and charges in workplace DC pensions, in response to the Office of Fair Trading (OFT) review into the workplace DC market. This includes a duty on governance bodies – namely trustees and Independent Governance Committees – to report on the level of transaction costs in their schemes.

These governance bodies have a duty to request and report on transaction costs as far as they are able. Without a matching duty on asset managers to provide full disclosure of these costs in a standardised form, trustees and IGCs may not be able to perform their function of assessing whether scheme members are receiving value for money.

As there is no standardised disclosure for reporting information about some types of transaction costs, the FCA has consulted on plans to set standards to provide clarity around these costs. This is intended to deliver consistency and give governance bodies confidence that the information presented to them contains a comprehensive assessment of the costs that are incurred on their behalf by asset managers. What are transaction costs?

The FCA has broken transaction costs down into a number of broad categories. These relate to costs for money going into and out of the scheme from members making contributions or leaving the scheme, as well as transaction costs arising from investment switching decisions, made by either individual members, the trustees or provider, or the scheme’s investment managers.

What has the FCA decided?

With effect from 3 January 2018, in response to a request from the governance body of a relevant pension scheme, asset managers must provide:

- information about transaction costs calculated according to the ‘slippage cost’ methodology;

- information about administration charges; and

- appropriate contextual information.

Where asset managers do not have the relevant information, they must seek it from other firms, and those other firms, where they are FCA authorised, must provide the information.

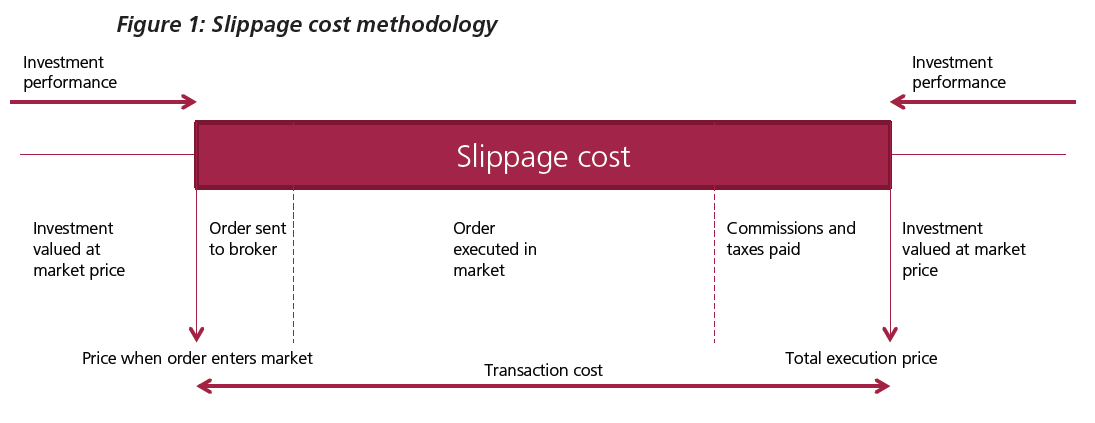

The Slippage Cost

The slippage cost methodology compares actual prices with the value of the asset immediately before the order to transact entered the market. This concept is the basis of most models of transaction cost analysis, and only needs two pieces of basic information for each transaction:

- The actual execution price (which should be a matter of record in an accounting system).

- The time an order enters the market (which should be captured by an order management system, and which it is a requirement of the Markets in Financial Instruments Directive (MiFID) to record16). This time can then be used to identify the mid-market price of the asset, called the ‘arrival price’; this can then be compared to the execution price.

The FCA’s consultation document set out how this works in practice:

What’s next?

The FCA is working with the DWP on the next steps. It understands that the DWP is planning to consult on proposals as to how costs and charges relating to occupational pension schemes should be published and disclosed to scheme members. Subject to their final regulations coming into force, the FCA intends to consult in the second quarter of 2018 on its proposals to achieve similar outcomes for workplace personal pension schemes.

Comment

The drive to improve the clarity of charges incurred by pension schemes and members continues to grow. This is a common sense move by the FCA, as even if trustees and providers wish to provide details of their transactions costs, they can be prevented from doing so if there is no requirement on asset managers to provide this information in the first place.

As with every other initiative to de-mystify pension scheme charges in the last few years, this one requirement won’t stop the criticism of the pension scheme charging structures, but it is another step in the right direction.